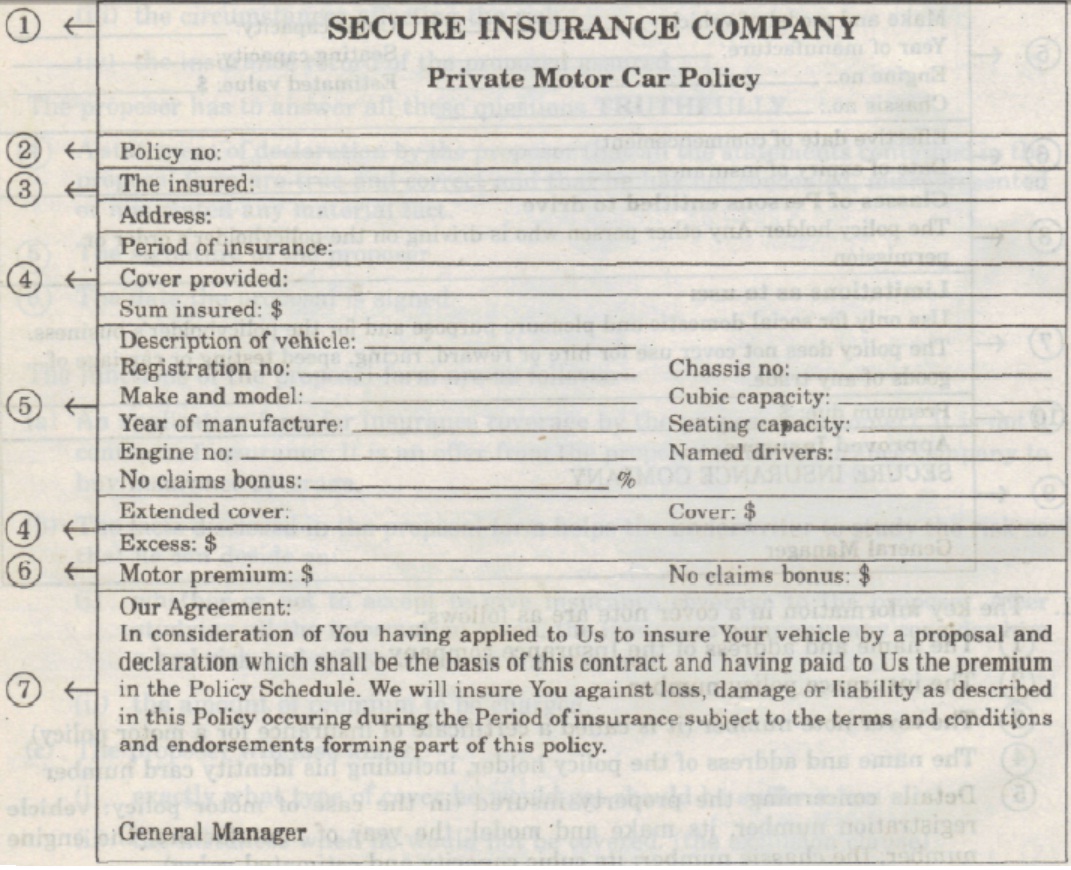

Important

of Insurance

Every individual

business faces risks. It could

be the risk of loss and damage to property, vehicles and stock due to fire,

burglary, flood, accident and even theft by its own employees. It could be the

risk of being sued for claims by members of the public, its customers and even

by its own employees due to damages and losses suffered by these people as a

result of its negligence. It could also be the risk of financial loss due to

bad business decisions or unanticipated changes in demand for the business' goods.

In return for a small premium, insurance

underwriters are willing to offer a wide variety of insurance cover (see Types of Insurance) to the ordinary business to protect it against some of these eventualities. Should the insured risk occur, the business will be

indemnified and protected?

It must be

realized, however, that not all risks faced by the business is insurable. Some,

such as loss due to bad business decisions and unanticipated changes in demand,

are non-insurable. The insurance

premiums collected by the various insurance companies in the country forms a

very important pool of liquid funds in

the country. Apart from setting a certain proportion aside to meet the claims of those who do

eventually suffer loss as a result of the insured risk occurring, the rest of

the funds provide an important source

of finance for the development of the national economy which are shown

on the figure on the next page:

(a) Invested in shares in industry and

commerce, at home or abroad;

(b) Lent out to businesses and families for

example to purchase property;

(c) Lent out to central governments and local councils.

Insurance is of

particular importance to the UK. Sale of general and life insurance policies of

British Insurance companies abroad via overseas branches forms a very important

part of her (UK) invisible exports. The repatriation of interest, dividends and

profits from these overseas branches back to the UK also helps in her Balance

of Payments.

Insurance is a pooling of risks to enable people to

share risks. In life, everyone including businessmen, faces risks, resulting in

losses. Any loss due to the insurer's risk materializing will be compensated for out of the common

pool. The amount of compensation will be just enough to indemnify or restore the insured to the position he was in

immediately before the loss. The indemnity will not exceed the amount

originally insured for. The insurance company will have to study the risk

involved for each insurance proposal. It will consider all factors that may

make the insured risk more likely to happen. The basic principle is: The higher the risk, the higher the premium

charged. The premium finally payable by the insured can be calculated

based on:

(a) The insured value of the

property;

(b) The tariff rate or the rate

of premium quoted by the insurance company.

Illustration

After studying the risks involved

for a certain proposal for fire insurance, the insurance company quoted a rate

of 20 cents per $100. Suppose the value of property was $100,000, the total

amount of insurance premium payable would be:

Rate quoted to insure property

against fire 20 cents per $100

Insured value of property

$100,000

Amount of premium payable 0.20 x 100,000 = $200

100

The premium payable ($200 per

year) is so small compared to

the amount of possible compensation payable, i.e. $100,000. 'This is because

the total number of people who face the risk of loss due to fire is very great.

It incorporates all owners of properties in the country. Therefore, the number

of those who are willing to contribute to the central pool is very great.

Consequently, the central pool is very

big even though each insured pay a small premium. But only a small percentage of the total population

who buys fire insurance will eventually suffer a loss. So, it is possible to

pay the few unfortunate from the central pool. It is a case of the fortunate

many (who did not suffer any loss due to fire) who help the unfortunate few

(who did suffer a loss due to fire). This is the whole principle of 'pooling of

risks'.

How

Insurance Company Make Profit?

Insurance underwriters are in

business providing an essential service to the public. In return, they hope to

make a profit for their shareholders. Insurance

underwriters sell insurance cover to their clients in return for insurance premiums. In order to reduce

competition amongst themselves and to introduce stability into the business,

they have introduced uniform practices such

as adopting standard tariffs or rates of premium and standard forms of policy,

especially in fire insurance. The proper

management of funds will ensure that while there is sufficient liquid funds

out of which claims can be promptly paid, the rest of the funds will be

skillfully invested to earn an income in excess of their expenses so that the

insurance company will make a profit.

Insurable

and Non-Insurable Risks

Insurers (i.e. insurance

companies and insurance underwriters) will only undertake to cover anyone

against insurable risks. Insurable

risks are those whose chances of occurring can be mathematically calculated by statisticians and actuaries from

available statistical records. The calculated risk is then used as a basis for

computing the premium to be charged. This must be high enough to ensure that

the insurance company will not run at a loss in the long run, in order to meet

the various claims from the central pool. The insurer is able to cover such a risk

because:

a) A

large number of people who are subjected to the risk, are willing to pool their

risks, by contributing premiums to a central fund;

b)

Only

a small number actually suffers loss;

c)

Claims

in the long run are less than the funds available to meet them.

Examples of

insurable risks are perils at sea, fire, burglary, personal liability, motor accident

and flood. Some risks are non-insurable because it is not possible to calculate

the chances of their occurring as no statistical records of their occurrence

are available. Hence, no insurer can calculate the premium. Examples of

non-insurable risks are war and trade risks like business losses due to bad management,

failure of demand, rise in costs, changes in fashion and bad debt.

Over-Insurance

A man insures

his property which is worth only $10,000 for $12,000. It is NOT to his

advantage to do this because:

(a)

He

has to pay a higher premium than

otherwise necessary.

(b) He can NEVER get

$12,000 even if his property is totally destroyed. The maximum compensation is

only $10,000 since insurance is a contract of indemnity.

(c)

He

should not knowingly over-inflate the value of his property since insurance is

a contract of utmost good faith.

Under-Insurance

A man insures

his property which is worth $10,000 for $8,000. He hopes to save on the

insurance premium since he will be paying a lower premium. However,

under-insurance is also not advantageous to him because:

(a)

His

property is not fully covered. If it is totally destroyed, the maximum

he could get is only $8,000, since premium is only paid for $8,000. If half of

the property is destroyed, the amount he would receive as compensation would be

half of the amount covered (i.e. ½ of $8,000), i.e. $4,000 even though the

replacement value of the property destroyed is 5,000. This is because insurance

is a contract of indemnity.

(b) He should not

knowingly deflate the value of his property since insurance is a contract of utmost good faith.

Principles

and Doctrines of Insurance

These

fundamental principles ensure that the whole basis of insurance — the pooling

of risks — runs properly. The insured would not be able to defraud the insurer

who will in turn be able to fulfill their obligations as contained in the

insurance contract.

1. Insurable Interest: This applies to

all contracts of insurance. We may only insure those things in which we have insurable

interest. To have insurable interest in something is to be in danger of

suffering loss or incurring some personal liability should the thing be

destroyed or damaged in any way or to be able to derive benefits

from its preservation. Examples:

(i)

I cannot insure my neighbor's house and property

since I have no insurable interest in them.

(ii) I can insure my

own –V property, house, life, even my spouse's life or the life of the man who manages

my business as I have insurable interest in these things.

(iii) I can insure my

stock stored in a rented premises against fire although I cannot insure the

premises (building) itself.

(iv) A creditor may

insure the life of his debtor up to the value of the amount owed.

2. Utmost Good Faith: This applies to

all contracts of insurance. The insured must disclose fully all material facts known

in answering all questions in the proposal form and in all dealings with the

insurance company. The insurance company must be informed of factors that are

likely to increase the chances of the insured risk occurring because it will

base the computation of the premium on the truth of the information supplied. Failure

to disclose the whole truth will make the policy void and the insurance company

will refuse to pay compensation should a loss occur. Example: When 1 apply to

insure my premises against fire, it is my duty to inform the insurance company

if my premises contains goods which are inflammable.

3. Indemnity: This Applies to all contracts of

insurance except life assurance and personal accident insurance. To indemnify'

means to restore a person to the position that he was in immediately before the

event concerned took place. Thus, all compensation to the insured who had suffered

a loss would be to indemnify him, and NOT to allow him to make a profit out of

his misfortune. Life assurance and personal accident policies are not contracts

of indemnity because it is not possible to restore the dead to life, or to

restore an amputated leg for instance, to one who has met with an accident. Instead,

a lump sum called the 'benefit' is paid to the beneficiary. Examples:

(i)

A new motor car was insured for $100,000.

After 6 months, it was totally wrecked in a motor accident.

(ii)

The owner would be paid compensation in the form of

a sum of money which will enable him to buy a 6 month-old car of the same make,

that is, depreciation on the car would be considered. If the current market

value of such a car is $85,000, then the owner would get a compensation of $85,000.

This is sufficient to indemnify him.

(iii) Mr X insured his

stock against fire for $3,000. One-third of it was destroyed. Even if the replacement

value of the stock destroyed was $1,100, Mr X, would only receive a

proportionate compensation of $1,000 (1/3 of $3,000) as he had paid premium

based on $3,000. If the replacement cost of the stock destroyed is $900,

then Mr X would be reimbursed $900 even though he had paid a premium based

on the higher figure. If Mr X's stock 5 p was totally destroyed, the maximum

compensation he could get would be only $3,000 even though the replacement

value might be $3,300.

- The First

Corollary of Indemnity — Contribution: This applies to all contracts of insurance

except life risks. Contribution' applies where a person has insured identical risks

on the same property with a number of companies, or when policies overlap. The

amount of the loss is shared proportionately between the insurance companies.

Examples:

Ø Suppose

Mr A insures his goods worth $1,000 against fire for $1,000 each with 3

insurance companies. In the event of a loss due to fire, Mr A would receive a

maximum of $1,000; each of the insurance companies paying $333V3. He cannot

receive $1,000 from each insurance company, or he would be making a profit.

Ø However,

should Mr A insure his life for $100,000 each with three insurance companies,

his next-of-kin can receive $300,000 altogether should he pass away. This is

because life policies are NOT policies of indemnity

- The Second

Corollary of Indemnity — Subrogation: This means that when the insurance

company has paid out the claims, it 'subrogates' or steps into the place of the

insured and inherits all his rights and remedies against third parties. Example:

Ø Mr

A's car was wrecked in an accident. He agreed to accept $4,000 in settlement as

indemnity. The wreck is then sold to a junk yard for $50. Mr A loses all rights

to this amount because the insurance company, after paying him, is now the owner

of the wreck. The $50 therefore goes to the insurance company.

4. The Doctrine of Proximate Cause: This applies to

all insurance contacts. The root cause of the event is known as the proximate cause.

This means that the insured will only be compensated if his loss was caused

directly by the risk he has insured against. If the immediate cause of the loss

was due to risks specifically excluded by the insurance policy, then no claim

can be made. Examples:

(i) I insure my

stock against floods. It is destroyed by flood waters. This is an insured

peril. I am therefore entitled to claim compensation form the loss incurred.

(ii)Suppose the

policy specifically excludes floods because my warehouse is near a big sluggish

river which is very susceptible to over-flooding its banks with every heavy

downpour. If flood is clearly the direct cause of the loss, then no claim can

be made.

(iii)Similarly, Mr B

may take a personal accident policy. One day, while driving, he had an accident.

Because of the shock, he died of a heart attack. The insurance company may not

pay because the root cause of his death was not due to the accident — but a heart

attack.

Effecting

an Insurance Policy

The buyer (or

proposer) may either approach an insurance company direct, or alternatively may

seek the assistance of an insurance agent or an insurance broker. The buyer

will have to complete a standard proposal

form which contains questions or instructions designed to obtain

information regarding the property or the person for which/whom insurance is

sought. All material facts known by the buyer must be disclosed otherwise the

contract of insurance may be declared null and void. Based on the information

given in the proposal form, the insurance company will study the risk involved

and then decide on the premium and the proportion of the risk it is prepared to

absorb. Bad risks will not be accepted by the company. For life assurance policies,

the client may sometimes have to pass a standardized medical examination before

the company accepts him. Normally, a risk is absorbed by a large number of

underwriters. When the whole risk is covered and the premium collected, a cover

note is issued to the

client. This is evidence of an insurance contract. For life policies, no cover

note is issued. Rather, the binding receipt of premium issued by the insurance

company is evidence of the insurance contract. The insurance company then

issues the client with an insurance

policy which is really the legal contract between the insured and the

insurance company.

Procedure

in Making a Claim

For a claim in

an insurance policy to be valid, the insured must follow certain procedures. Failure

to observe the instructions set down by the insurance company will prejudice

the claim. Below is an example of a typical procedure for a marine insurance claim

in the event of loss or damage to cargo. The principles involved are essentially

the same for other types of policy as well.

1. The

insured must inspect the goods before taking delivery if the loss or damage is apparent,

or as soon as the loss or damage is discovered.

2. The

insured must then inform the insurer immediately, and request for a survey of

the goods by the underwriter's agents or the surveyors named in the policy or

insurance certificate. It is important that the condition of the goods and its

packing must not be tampered with until the surveyor arrives. However, the

insured may take steps to ensure that there is no further damage to the goods. In

the case of a claim under other types of policies, say, motor, the insured must

inform the insurance company immediately of the event of the loss. He must also

make a report to the police within 24 hours after the accident. The police will

make an independent report after its investigation as to the probable cause of

the event. The vehicle will have to be towed to a workshop approved by the

insurance company.

3. The

insured must also request ship-owners, other carriers, forwarding agents,

Customs, the Port Authority and other bales to be present for a joint survey.

It is their responsibility to certify any loss or damage to preserve the

insurance companies' rights against third parties. If the latter is found to be

guilty of negligence, the insurance company can then sue them for damage or

loss incurred.

4. Notice

of the loss or damage must be made in writing to the bailees within the time limit

prescribed.

5. Together

with his claim form, the

insured must submit certain documents to substantiate his claim:

(a)

To

prove insurance — original copy of the policy or certificate of insurance

(b) To prove ownership

(i)

bill of lading (for cargo)

(ii) vehicle ownership card (for

motor)

(iii) charter party

(c)

To

prove value

(i) Invoices

(ii) Packing lists

(d) To prove loss/damage

(i) Survey

report

(ii) Landing/general

survey report

(iii) Sales receipt

(e) To enable the insurance company to

make claims on third parties

(i) The police report

Reference:

Betsy, L., & Tan, K. S. (1999). Insurance., Modern certificate guide: Elements

of Commerce (pp.216-223). Singapore: Oxford

University Press.

{kind=link}